Mitch Verhelle

About Me

Hey there! I'm Mitch, and I'm really into mathematical modeling, especially in the world of quantitative finance. I studied computer science and math at Cornell University, and now I'm working on my Master of Science in Financial Mathematics at The University of Chicago.

In my program, I'm learning to use my math and computer science skills in the quant trading industry. I enjoy using math tools to turn specific trading issues into broader insights and come up with innovative strategies to navigate the ever-changing world of options trading.

Outside of class, you'll usually find me diving into different math activities, from learning about AI models to solving probability puzzles to staying updated on the latest trends in quantitative finance. If any of my hobies resonate with you and you'd like ot talk, feel free to reach out—I'm always up for a good conversation!

By the way, this video is my current favorite YouTube video called How to train simple AIs to balance a double pendulum by Pezzza's Work. You should check it out if you have some extra time, the strategy he uses to train his model is something I want to start trying with my own projects.

Heart Condition Predictor

This competition was hosted as extra credit for students enrolled in CS4780 in spring of 2024. The competition provides a dataset of anonymized medical statistics and asks participants to develop a model that will predict if the patient will get heart disease. I placed 7th out of 129 teams. I developed a few models, my most successful being adaboost logistic classification model using an elastic net, in addition to ample data preprocessing to achieve my ranking. For more information, please click the button below to request access to the GitHub repository.

Request Access

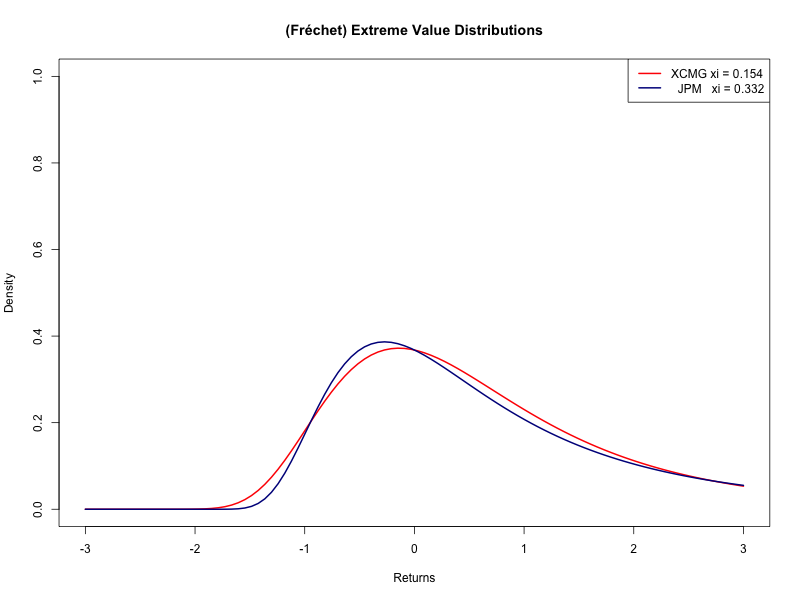

Extreme Value Shape Parameters for XCMG and JPM stocks:

A Comparitive Analysis

I select two stocks from Yahoo Finance, XCMG and JPM. I then analyze the extreme value distribution shape parameter of these returns to provide insights into extreme value modeling for these returns. This allows me to theorize about how to approach risk for hypothetical investment portfolios involving either of these stocks. I develop and employ a robust framework for estimating the shape parameters of the financial gains and losses of both stocks by looking at financial returns over a 5-year period. The methods used in this project were learned from Cornell University’s ORIE 4565 Extreme Values in Finance course, taught by Professor Gennady Samorodnitsky in Spring 2024.

Chess Puzzle AI Project on GitHub

This project evaluates the performance of two chess AI trained on chess puzzles against Stockfish, the current best open-source chess engine. We used LiChess's open source chess board database to evaluate our models. We developed a user interface to allow players to play themselves, watch each AI play, or evaluate the AI performance according to various evaluation metrics. The text-input is parsed into keywords using ChatGPT tokens to allow users to hand-select puzzles using keywords. This is my final project for my computer science AI course, CS 4701 AI Practicum, taught by Bart Selman. Source Code.

Contact

Feel free to reach out by clicking the "Email" hyperlink below or sending a message to mitch@verhelle.com